Architecture

FINSABER separates the reusable backtesting framework from research strategy implementations. The package boundary is the backtest package; examples, LLM agents, RL agents, and experiment launchers remain repository-level research code.

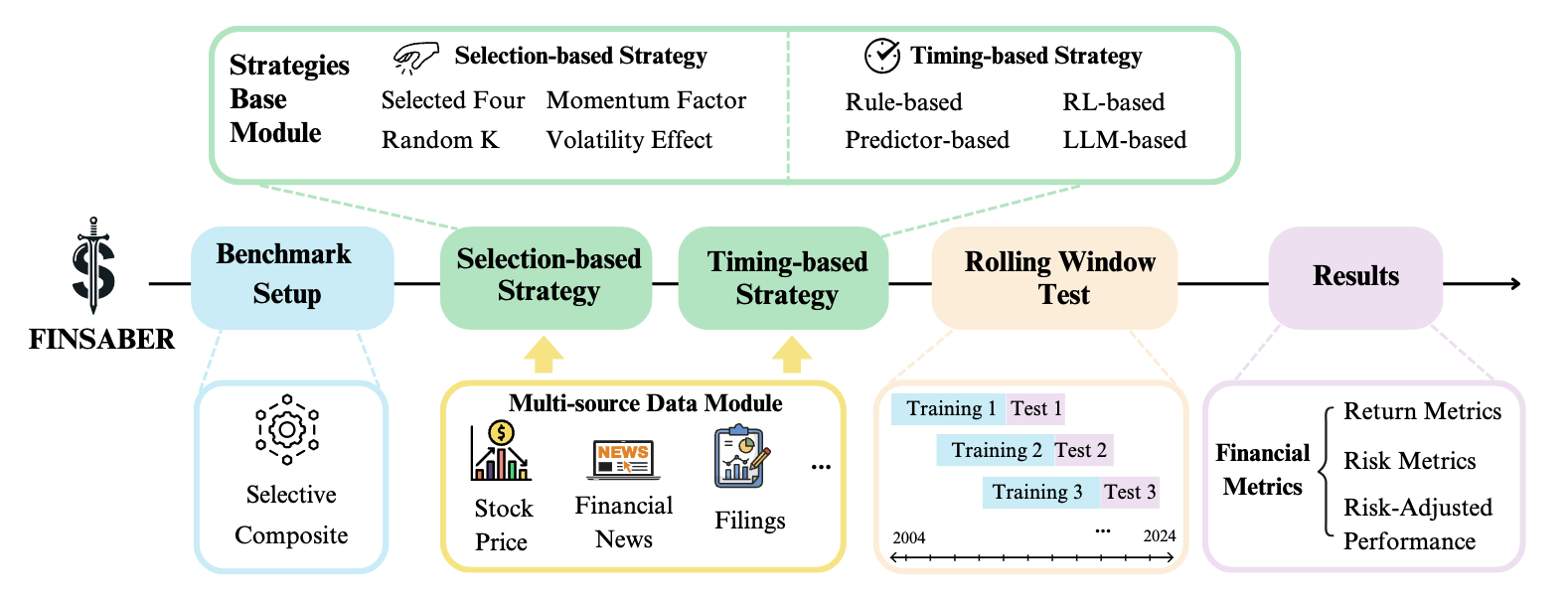

Framework Figure

Core Flow

flowchart TD

A[Dataset files or custom source] --> B[TradingData adapter]

B --> C[TradeConfig]

C --> D{Engine}

D --> E[FINSABERBt Backtrader path]

D --> F[FINSABER Python-native path]

E --> G[Strategy signal]

F --> G

G --> H[Execution timing]

H --> I[Adjusted price selection]

I --> J[Commission, slippage, liquidity cap, LLM cost]

J --> K[Portfolio state]

K --> L[Metrics]

L --> M[ResultWriter artifacts]TradingDataprovides date-indexed market data and optional modalities such as news, filings, and earnings calls.TradeConfignormalizes run parameters, including tickers, date range, cash, execution timing, costs, liquidity controls, and result output paths.FINSABERBtorFINSABERiterates through tickers, windows, or selected universes.- Strategies read only the data exposed for the current decision point.

- Execution utilities apply timing, adjusted prices, commission, slippage, and liquidity caps.

- Metrics and artifacts are written to a structured run directory when

save_results=True.

Engines

Use FINSABERBt for Backtrader-compatible strategies. It converts loader output into Backtrader feeds, configures broker costs, runs each ticker or window, then extracts broker/analyzer results.

Use FINSABER for Python-native strategies and LLM-style agents. It exposes daily data to strategy on_data logic and routes orders through BacktestFrameworkIso, which controls fills, position updates, rejected orders, and cost accounting.

Choosing an engine

Use FINSABERBt when your strategy already follows Backtrader's next() loop. Use FINSABER when an agent needs direct access to daily dictionaries containing price, news, filings, or extra modalities.

Package Boundary

The installable package exposes stable framework pieces:

backtest/

data_util/ TradingData adapters

toolkit/ config, execution, metrics, result writing, LLM cost tracking

strategy/ reusable base strategies and selectors

finsaber.py Python-native engine

finsaber_bt.py Backtrader engine

Paper-specific integrations such as FinMem, FinAgent, FinCon, and FinRL live outside the core package. They can depend on public APIs, but the package should not import them at module import time.

Correctness Principles

Backtests should state when a decision is made and when an order fills. For date-level features, prefer execution_timing="next_open" because news and filings usually do not have reliable intraday availability. Use adjusted OHLC for split-adjusted simulation, but retain raw volume for liquidity limits. Liquidity and rolling statistics must use prior bars only.

Bias controls

Do not rank tickers, compute liquidity, or construct features from data outside the current training or decision window. If exact announcement timestamps are unavailable, treat date-only text as available from the next decision point.

Extension Points

Add new datasets by implementing TradingData. Add new strategies by subclassing the appropriate base strategy. Add new execution assumptions in backtest/toolkit/execution.py and expose them through TradeConfig so the assumption is visible in saved run configuration.