Financial backtesting, made explicit.

A package-oriented framework for evaluating strategies over prices, news, filings, and extensible market data with clear timing, adjustment, liquidity, slippage, and LLM-cost assumptions.

FINSABER

FINSABER is a research framework for evaluating financial trading strategies over price, news, filings, and extensible market data. FINSABER-2 upgrades the original FINSABER code into a package-oriented backtesting framework with explicit execution assumptions and structured result artifacts.

Framework Highlights

Beginner concepts

Learn signals, orders, fills, positions, equity curves, timing, and common backtesting biases.

Pluggable market data

Use the built-in parquet and dictionary loaders, or implement TradingData for private datasets.

Explicit execution

Choose next_open or same_close, adjusted prices, commission, slippage, liquidity caps, and LLM costs.

Strategy extension points

Run Backtrader strategies, Python-native agents, LLM loops, and rolling-window ticker selectors.

Structured results

Analyze stable CSV and JSON artifacts for metrics, trades, orders, equity curves, rejected orders, and costs.

Recommended Reading Path

If you are new to the framework, read in this order:

- Backtesting Concepts for finance and backtesting vocabulary.

- Quick Start to run a short buy-and-hold example.

- Configuration to understand every important run setting.

- Data and Strategies when plugging in your own dataset or model.

- Execution Model and Results before interpreting performance.

The installable wheel intentionally focuses on reusable backtesting infrastructure. Paper-specific FinMem, FinAgent, FinCon, and FinRL integrations remain available in the repository, but the package exports data loaders, execution models, metrics, result writers, selectors, and strategy interfaces.

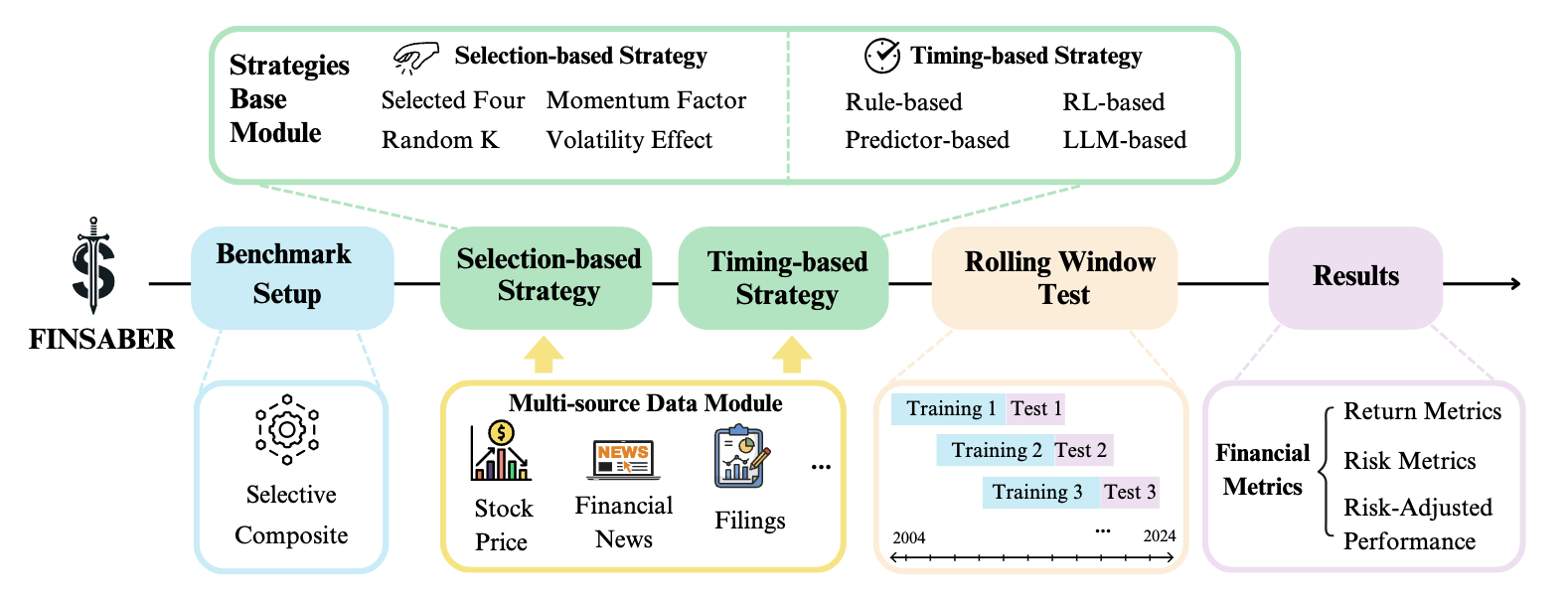

Workflow

The repository includes the original FINSABER pipeline figure:

At the framework level, the upgraded backtesting path follows this lifecycle:

flowchart LR

A[TradingData] --> B[TradeConfig]

B --> C{Engine}

C --> D[FINSABERBt]

C --> E[FINSABER]

D --> F[Strategy decisions]

E --> F

F --> G[Execution model]

G --> H[Metrics and artifacts]The dataset implements TradingData, the config defines the market universe and execution assumptions, the engine iterates through dates and tickers, the strategy emits decisions, and the execution layer applies fills, costs, liquidity constraints, and metrics. See Architecture for the detailed lifecycle.

Start Quickly

from finsaber import FINSABERBt, FinsaberParquetDataset

from finsaber.strategy.timing import BuyAndHoldStrategy

data = FinsaberParquetDataset(r"I:\Data\finsaber2\sp500_2000_2025_parquet")

config = {

"data_loader": data,

"tickers": ["AAPL"],

"date_from": "2024-01-02",

"date_to": "2024-01-10",

"setup_name": "demo",

"execution_timing": "next_open",

"save_results": True,

"silence": True,

}

results = FINSABERBt(config).run_iterative_tickers(BuyAndHoldStrategy)

print(results["AAPL"]["total_return"])

Engines

Use FINSABERBt for Backtrader-compatible timing strategies and baseline technical strategies.

Use FINSABER for Python-native or LLM-style strategies that consume date-level data and submit orders through the framework object.